All Categories

Featured

Table of Contents

Additionally, as you handle your policy throughout your lifetime, you'll want a communicative and clear insurance supplier. In contrast to an entire life insurance plan, global life insurance coverage offers versatile costs settlements and has a tendency to be less expensive than an entire life policy. The main drawbacks of universal life insurance coverage plans are that they call for maintenance, as you should keep track of your policy's cash money value.

Indexed Universal Life Leads

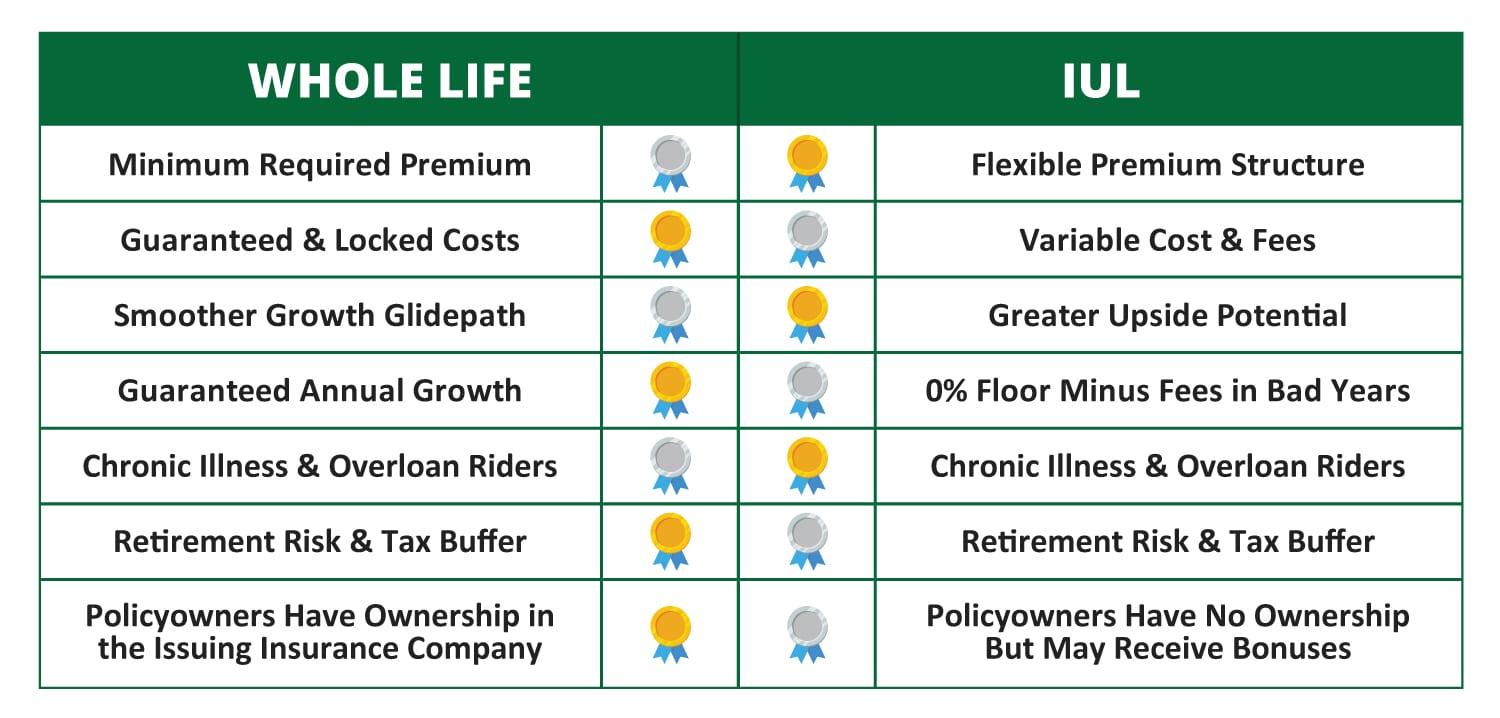

Neither whole life or universal life insurance policy is far better than the other. Universal life insurance policy might attract those looking for long-term insurance coverage with adaptability and higher returns.

Our work is to provide the most extensive and trusted info so you can make the best choice. Our round-ups and testimonials normally are composed of reliable business. Financial toughness and client satisfaction are trademarks of a credible life insurance coverage carrier. Financial toughness demonstrates the capability of a firm to stand up to any economic circumstance, like a recession.

Availability is also a main element we analyze when examining life insurance policy companies. Accessibility refers to a policy's affordability and inclusion of those in various risk classes (health and wellness categories, age, lifestyles, etc).

We utilize a firm's web site to assess the expansiveness of its product line. Some business provide an exhaustive checklist of long-term and short-term plans, while others only give term life insurance policy.

Is Iul Insurance A Good Investment

If your IUL policy has ample money value, you can obtain versus it with versatile payment terms and reduced rates of interest. The option to design an IUL plan that mirrors your specific requirements and scenario. With an indexed universal life plan, you allocate premium to an Indexed Account, thus developing a Section and the 12-month Segment Term for that section begins.

At the end of the sector term, each segment earns an Indexed Credit rating. An Indexed Credit rating is computed for a segment if value remains in the section at section maturity.

These limitations are established at the beginning of the section term and are guaranteed for the whole sector term. There are 4 choices of Indexed Accounts (Indexed Account A, B, C, and E) and each has a different kind of limit. Indexed Account An establishes a cap on the Indexed Credit history for a section.

Best Performing Iul

The development cap will certainly vary and be reset at the beginning of a section term. The involvement rate establishes just how much of a rise in the S&P 500's * Index Value puts on sections in Indexed Account B. Greater minimum growth cap than Indexed Account A and an Indexed Account Cost.

There is an Indexed Account Cost related to the Indexed Account Multiplier. No matter of which Indexed Account you pick, your cash money value is constantly shielded from unfavorable market performance. Cash is moved at least as soon as per quarter into an Indexed Account. The day on which that occurs is called a sweep day, and this produces a Section.

At Section Maturation an Indexed Credit history is computed from the adjustment in the S&P 500 *. The worth in the Segment earns an Indexed Credit scores which is determined from an Index Development Rate. That development rate is a percent adjustment in the existing index from the beginning of a Segment up until the Section Maturity day.

Sections automatically restore for one more Segment Term unless a transfer is requested. Costs got considering that the last sweep date and any kind of asked for transfers are rolled into the same Sector to ensure that for any type of month, there will be a single brand-new Segment created for a provided Indexed Account.

Below's a little refresher course for you on what makes an IUL insurance policy different from other type of life insurance policy items: This is permanent life insurance policy, which is vital for firms who watch out for taking on even more danger. This is because the policyholder will have the insurance coverage for their whole life as it builds money worth.

Allianz Iul

Rate of interest is gained by tracking a team of supplies picked by the insurance firm. Danger analysis is an essential part of harmonizing worth for the client without threatening the firm's success via the fatality advantage. On the various other hand, most various other type of insurance coverage only expand their cash money value via non-equity index accounts.

Plans in this classification still have money worth development extra dependably because they build up a rates of interest on an established timetable, making it simpler to handle risk. One of the more versatile choices, this option is perhaps the riskiest for both the insurance company and insurance policy holder. Stock performance determines success for both the business and the customer with index universal life insurance policy.

While supplies are up, the insurance plan would certainly do well for the insurance policy holder, yet insurance firms need to regularly check in with danger assessment. Historically, this danger has actually paid off for insurance business, with it being one of the industry's most profitable markets.

For insurance firms, it's very vital to divulge that danger; customer relationships based upon trust fund and integrity will certainly assist business remain successful for longer, even if that company prevents a brief windfall. IUL insurance coverage policies might not be for everybody to build value, and insurance companies need to note this to their consumers.

Death Benefit Options Universal Life

As an example, when the index is performing well the worth escalates previous most various other life insurance policy policies. If we take an appearance at the plummeting market in 2020, indexed life insurance coverage did not enhance in plan value. This positions a threat to the insurance provider and especially to the policyholder.

In this case, the insurer would certainly still get the costs for the year, but the web loss would certainly be greater than if the proprietor kept their plan., which excuses an IUL insurance plan from similar federal laws for supplies and choices.

Insurance agents are not financiers and must describe that the policy must not be treated as an investment. After the COVID-19 pandemic, even more people obtained a life insurance plan, which boosted death threat for insurance providers.

To be successful in the extremely competitive insurance coverage profession, firms require to manage danger and prepare for the future. Predictive modeling and data analytics can aid set expectations.

Are you still not sure where to begin with an actuary? Don't worry, Lewis & Ellis are right here to direct you and the insurance coverage company via the procedure. We have actually created a collection of Windows-based actuarial software to assist our specialists and outdoors actuaries in efficiently and successfully completing a lot of their activities.

{kind=link}

Latest Posts

Indexed Variable Universal Life Insurance

Tax Free Retirement Iul

Universal Index Life Insurance Pros And Cons